Weekly industrial chain operation overview (04.16-04.23)

Views in this issue

(1) The WTI May contract approaching delivery on Monday hit a negative oil price. Although the market rebounded subsequently, it will still take time for supply and demand to balance. It is expected that short-term sharp rises and falls in international oil prices will become the norm.

(2) Polyester raw materials have followed the downward trend of oil prices this week. Recently, there has been a serious surplus of global crude oil, with delivery approaching and tank capacity tight, and the external crude oil plummeting, suppressing the sentiment of polyester raw materials. At present, terminal weaving orders have not yet recovered, and with the May Day holiday approaching, some weaving companies have plans to stop work and take holidays in advance. The terminal demand is not good, and the bottom of polyester raw materials is expected to be weak and volatile in the short term. Focus on the impact of the recent macro situation on market conditions.

(3) The polyester yarn market’s production and sales this week were relatively average, with production and sales exceeding 100 on Thursday alone. Crude oil has plummeted, the market has a strong wait-and-see sentiment, and bargain hunting is cautious. All links in the industry chain are facing greater sales pressure and may face greater challenges in May. And with the May Day holiday approaching, some weaving companies have plans to stop work and take holidays in advance. Polyester yarn prices are expected to remain weak in the short term. Focus on macroeconomics, changes in terminal demand, crude oil and PTA trends.

Polyester factory polyester yarn operation overview

The overall production and sales of polyester yarn this week were light. Only on Thursday, driven by the rebound of polyester raw materials, the production and sales exceeded 100%. Before demand recovers effectively, polyester inventory is simply transferred to the weaving process and becomes raw material inventory, and the terminal weaving industry is still in a downward cycle. In the medium term, it may be difficult to see substantial changes in demand. As of April 23, it is estimated that polyester yarn factories in Jiangsu and Zhejiang will have 18 to 27 days of inventory. It is expected that polyester yarn prices will be weak and volatile in the short term.

In terms of production efficiency, the price of polyester yarn continued to fall this week, approaching the lowest point in the previous period. The overall profit margin of theoretical cash flow of various categories of polyester yarn was compressed, and the losses of FDY and POY expanded.

Semi-glossy slice price trend

Due to the large increase in the previous period, the price of semi-glossy slices fell sharply by more than 9% this week. Slicing theory cash flow also narrowed significantly. Slice prices are expected to remain weak in the short term. In the later period, we will focus on the trend of polyester raw materials, device dynamics and changes in downstream demand.

Transaction status of China Textile City

The transaction volume of China Textile City from 04/17 to 04/23 totaled 53.36 million meters, an increase of 1.79 million meters from last week, of which 36.7 million meters of chemical fiber cloth were traded, an increase of 1.59 million meters from last week.

International crude oil weekly analysis

International oil prices have experienced the most turbulent week in history this week. U.S. crude oil futures for May delivery closed at minus $37.63 a barrel on Monday, experiencing the worst sell-off in history that day. Global benchmark Brent crude oil futures took a hit on Tuesday, hitting a 20-year low. Although U.S. oil rebounded by more than 40% on Wednesday and Thursday, fundamental supply, demand and inventories are still deteriorating further. Oil prices are expected to remain volatile in the short term. Focus on the international economic situation and geopolitical influences.

U.S. EIA crude oil inventories for the week

Fundamental positive factors:

1. Starting from May, Azerbaijan’s ACG oil field will reduce production by approximately 80,000 barrels per day to fulfill Azerbaijan’s commitment to OPEC + Commitments under the production reduction agreement; Iraqi Oil Minister Ghaban said that after the production reduction agreement is implemented, oil prices will gradually stabilize, and it is expected that oil prices will rise to US$50 per barrel by the end of this year. He predicts that Iraq’s oil revenue will decrease by 50% this year compared with the same period last year.

2. On Wednesday, Oklahoma energy regulators approved a production reduction agreement that allows drillers in the state to suspend operations, which is a regional oil group seeking bailout from state regulators. First victory achieved.

Fundamental negative factors:

1. U.S. Energy Information Administration (EIA) Data released on Wednesday showed that U.S. crude oil inventories rose sharply again and oil prices continued to fluctuate sharply. In the week ended April 17, crude oil inventories increased by 15.022 million barrels, higher than the previous expectation of 13.821 million barrels; refined oil inventories increased by 7.876 million barrels, higher than the previous value of 6.28 million barrels, far higher than the previous estimate of 13.821 million barrels.higher than the forecast of 3.687 million barrels.

2. Fisher Global Energy Consulting (FGE) predicts that global crude oil demand will drop by 11 million barrels per day in 2020.

Global oil producers such as the United States and Russia plan to cut production by 9.7 million barrels per day, but unfortunately, this number does not reach the expected production reduction of 30 million barrels per day. s level. The June WTI crude oil futures contract may suffer the same fate as the May contract.

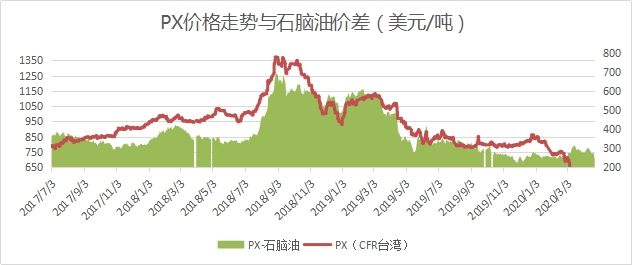

PX Price Trend

PX prices remained basically unchanged this week, while naphtha rose sharply by nearly 19%. There is no change in PX equipment this week, and the supply is stable. The trading atmosphere in the PX market was not high during the week, with bids being mostly offers and offers being deserted. Dragged down by falling costs and poor demand support, PX prices fluctuated within a narrow range this week and profits fell. Both domestic and external demand will be poor next week, and weaving starts will decline, making it difficult to find support on the demand side. It is expected that PX prices will be weak next week, operating in the range of 450-490 US dollars / ton CFR China. Focus on domestic PX installations, crude oil and PTA trends.

Polyester raw materials, PTA weekly trend

PTAfellabout5%thisweek.Crudeoilplummeted,marketsentimentwasfrustrated,PTAfundamentalswerenotfavorable,andfuturespriceshitnewlows.Recently,therehasbeenaserioussurplusofglobalcrudeoil,withdeliveryapproaching,tankcapacitytight,andexternalcrudeoilplummeting,suppressingsentimentintheNenghuasector.AsfarasPTAisconcerned,itsfundamentalsarenotfavorable.Onthesupplyside,underhighprocessingfees,PTA’soperatingratehasclimbedto93%,andsupplyisatahighlevel.Fromthedemandside,althoughthedownstreampolyesteroperatingratehasincreasedto84%,terminalweavingordershavenotyetrecovered,andwiththeMayDayholidayapproaching,someweavingcompanieshaveplanstostopworkearlyfortheholiday,andtheloomoperatingratehasdroppedto49%.Terminaldemandisnotgood,andtheincreaseinpolyesteroperatingrateislimited.PTAisinthestageofoversupply.AsoflastFriday,PTAsocialinventorywas3.35milliontons.Theinventorypressureisveryhigh,andthereisnoinflectionpointfordestocking.Thefuturespriceisunderpressure,anditisnotruledoutthatthefuturespricewillhitanewlow.Itisrecommendedtopayattentiontothemacroeconomicsituation,industrialchaindeviceload,andchangesinterminaldemand.

Polyester raw materials, MEG weekly trend

The price of ethylene glycol fell by about 2% this week, which was a relatively small decline. As of April 16, the overall operating load of domestic ethylene glycol was 58.83%, of which the operating load of coal-based ethylene glycol was 36.20%. The coal-based production load dropped to the lowest level in recent years. In addition to the shrinkage of domestic coal plants on the supply side, the volume of ethylene glycol arriving at ports continued to shrink in the first half of April, and the accumulation of ethylene glycol ports slowed down. Although there is no obvious improvement in the demand for ethylene glycol, due to the shrinkage of coal production on the supply side, the proportion of downstream procurement of oil products has increased, and the port shipment volume has increased slightly. In addition, the port arrival volume in the first half of April was not high. On April 20, East China The MEG port inventory in the main port area is approximately 1.253 million tons, a decrease of 4,000 tons from the previous period, and the ethylene glycol inventory has been slightly reduced. It is expected that the short-term trend of ethylene glycol may be slightly stronger than that of PTA. Focus on industrial operation and commodity atmosphere. </p