In 2018, the Shanghai International Energy Trading Center launched Shanghai Crude Oil Futures SC, which is China’s first crude oil futures contract and the world’s first RMB-denominated crude oil futures. The delivery target is the RMB bonded price of Middle East crude oil arriving at the port, and the target is to become the benchmark price of crude oil spot trade in Northeast Asia. The listing of Shanghai crude oil futures provides financial institutions with asset allocation tools and industrial institutions with hedging tools. It has performed well in the two years since its listing and has become the third largest crude oil futures in the world.

Positions have been steadily enlarged, and the entities have been continuously improved

March 2018 On the 26th, the first day of crude oil futures listing, positions were 1,779 lots and 42,000 lots were traded. Since then, the market has expanded steadily, with positions increasing by 45% year-on-year in 2019. International oil prices fluctuated significantly in 2020, and domestic crude oil futures positions also rapidly increased by more than three times in three months. As of March 25, 2020, SC’s total positions reached 115,000 lots.

SC has become the third largest crude oil futures in the world. From January to March 2020, the average daily positions of Brent/WTI/SC/Oman were 256/219/6/06,000 lots respectively, and the average daily trading volume was 116/157/8/06,000 lots. The holdings of Brent/WTI are 40/34 times that of SC. SC still has huge room for future development.

The participation of overseas investors in SC continues to increase. As of the end of 2019, the holding proportions of SC overseas/general legal persons/special legal persons were 20%/30%/30% respectively, and the trading volume proportions were 15%/25%/10% respectively. About two-thirds of the holdings of Brent and WTI come from production/trading/consumer companies, and about one-third of the holdings come from investment funds. At present, domestic spot hedging is still dominated by Brent. If some spot hedging positions can be returned in the future, it will help improve the SC participation structure.

Figure 1: SC’s trading positions have steadily increased since its listing

Data source :INE CITIC Futures Research Department

The overall valuation is reasonable, but there are differences in stages

The overall valuation is relatively reasonable. Using the DME Oman valuation system as a reference, the SC market price deviation is within ±3 US dollars/barrel more than 90% of the time. The main factors affecting the price fluctuation of Brent/SC include: RMB exchange rate, tanker freight, and the price difference between Brent and Dubai/Oman. Oil tanker freight rates rose sharply twice in October 2019 and March 2020, which had a significant impact on the internal and external price comparisons.

There is a short-term spread deviation. In addition to the influence of endogenous factors in the valuation system, delivery prices, capital operations, trading rules and other reasons may also lead to short-term deviations in the internal and external price differences. For example, the price spread fluctuated due to changes in market expectations before the delivery of the first-month contract SC1809 in August 2018, and the external market fluctuated significantly in March 2020. The internal market was unable to synchronize with the external market due to the price limit limit for two consecutive times, causing the price spread to deviate extremely.

The delivery function is good and the model is gradually mature

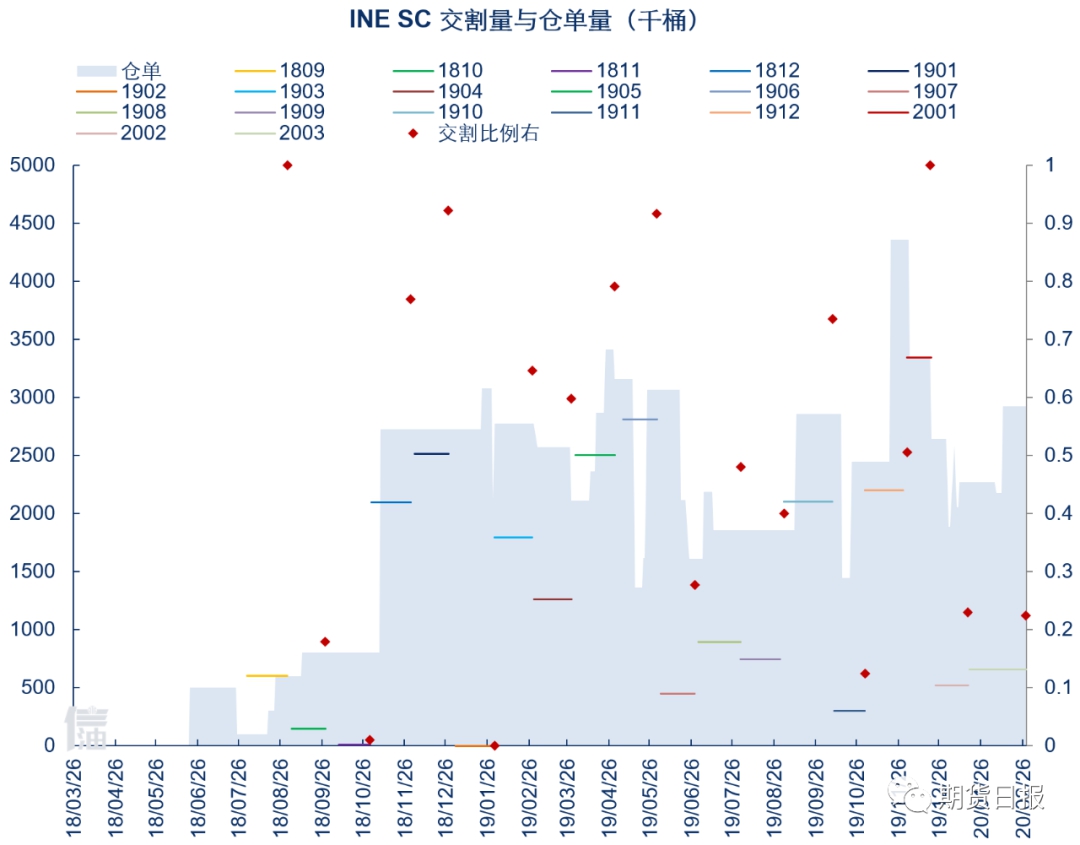

The delivery function is functioning well . Since SC’s listing, there have been a total of 16 deliveries, with a total delivery volume of 20.47 million barrels and a delivery amount of 9.1 billion yuan. The average delivery ratio of all contracts is about 50%, with SC1809 and SC1912 reaching 100% delivery rate.

Basra light oil is the main oil for delivery. Since the listing of SC, a total of 13.72 million barrels of registered warehouse receipts have been generated, of which Basra Light Oil/Oman Crude Oil/Upper Zakum/Qatar Offshore Oil have registered 932/350/50/500,000 barrels respectively. Basra light oil accounts for 68%.

PetroChina’s Dalian warehouse has the largest cumulative number of registered warehouse receipts. The cumulative registered warehouse receipts of CNPC Dalian/Sinochem Xingzhong/CNPC Zhanjiang/Shanghai Yangshan/Cezidao are 474/388/272/160/780,000 barrels. The oil delivered at PetroChina’s Dalian warehouse is mainly Oman oil, while other regions are dominated by Basra light oil.

Value preservation function is exerted, and industry exploration and participation

Upstream participation is relatively small few. The current main domestic crude oil producers are PetroChina, Sinopec, and CNOOC, which mainly supply refineries through internal settlement prices. About 80% of China’s crude oil demand comes from imports, domestic supply is limited, and its current participation in SC is relatively low.

Midstream operations are relatively mature. Crude oil traders are the main operating industry entities of SC. Crude oil hedging operations are relatively mature, and Lianyou, Lianhua, Sinochem, Zhenhua, some foreign-funded enterprises and private refineries have all begun to conduct hedging/arbitrage operations through SC. The long-term correlation of refined oil products is high, but deviations may occur in the short term, and the operating model still needs to be explored.

Downstream initial attempts have begun. As oil prices fell back to lows in 2020, some airlines and freight companies also began to try to buy and maintain value through SC. In the future, as SC operations become more mature, more industrial and institutional investors will participate to jointly support the development of Shanghai crude oil futures. (Author’s unit: CITIC Futures)

Figure 2: Review of SC’s delivery situation since its listing

Data source: INE CITIC Futures Research Department

</p